Humanoid Robots Are Now Shipping to BMW and Amazon Warehouses

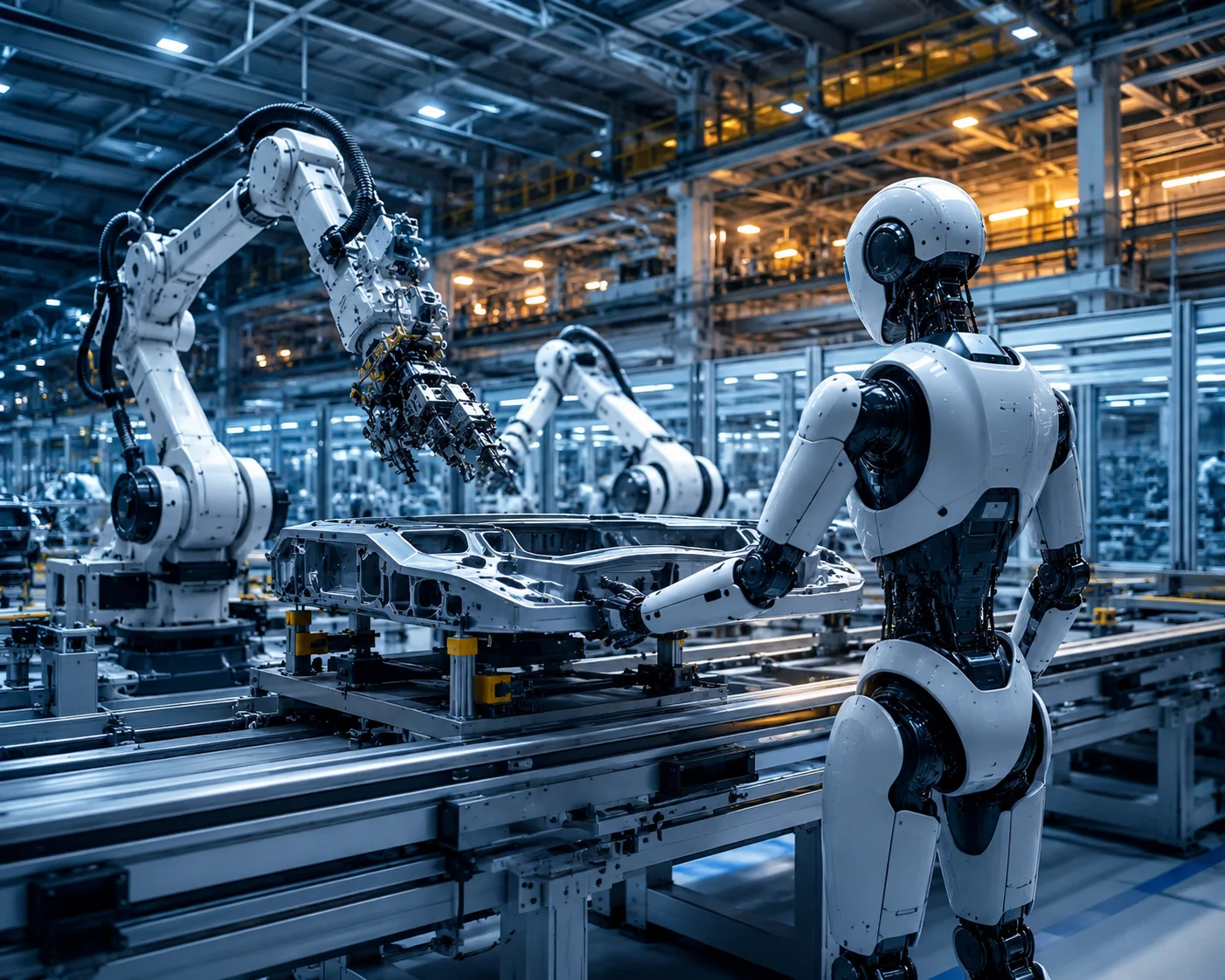

Figure AI’s humanoid robot Figure 02 is handling body shop parts transfer tasks at BMW’s Spartanburg, South Carolina manufacturing plant — the first commercial deployment of a general-purpose humanoid robot in a major automotive facility. Alongside Amazon’s continued rollout of Agility Robotics’ Digit platform in US fulfillment centres, 2026 marks the year in which humanoid robots moved from demonstration stage to production stage, with combined active deployments across both programmes measured in the hundreds of units rather than the dozens. The transition from lab to warehouse has happened faster than most industrial automation analysts forecast, and more slowly than the promotional projections from every company involved. Figure AI’s deployment announcements confirm production-status robots operating in a live automotive environment — a milestone that distinguishes genuine commercialisation from the controlled demonstrations that characterised the category through 2024.

The context for why this matters starts with what humanoid robots can do that fixed-arm robotics cannot. Industrial automation has been effective for decades in structured, repetitive tasks where the robot can be precisely positioned relative to a fixed workpiece: welding, paint application, conveyor transfer, press operation. The limitation of fixed-arm systems is that they require the environment to be designed around them — the workpiece must arrive at a predictable location, in a predictable orientation, within a predictable time window. Humanoid robots with bipedal mobility and multi-axis hand dexterity can operate in environments designed for humans: they can move between workstations, pick objects from varied positions, and handle tasks that change in sequence without requiring the facility to be rebuilt around the robot. This capability addresses exactly the category of tasks — dexterous, mobile, variable — that has resisted automation for decades not because of cost but because of engineering feasibility.

Figure 02 at BMW and What the Deployment Actually Does

The BMW-Figure deployment is not a general-purpose factory assistant. Figure 02 at Spartanburg is performing a specific defined task: transferring sheet metal body parts between storage racks and assembly stations. The parts are picked from a shelf location, carried across the facility floor, and placed at a specific position for the next stage of the assembly process. Human workers previously performed this task as a dedicated role; the deployment substitutes the robot for that specific workflow while human workers remain responsible for adjacent tasks that require judgment, adaptation, or quality inspection.

The commercial terms of the Figure-BMW arrangement have not been publicly disclosed, but the structure follows an emerging pattern in humanoid robot commercialisation: robots as a service (RaaS), where the manufacturer charges per-unit per-month for robots, software, maintenance, and remote monitoring rather than selling hardware outright. Per-unit monthly costs in this model are estimated at $8,000-$15,000 per robot per month, which prices the technology above the direct labour substitution threshold for low-wage markets but within range for high-labour-cost environments like Spartanburg, where assembly technicians earn $50,000-$70,000 annually in fully loaded cost terms. The economic logic is not blanket labour replacement but targeted substitution of the highest-repetition, lowest-skill-ceiling tasks in a facility that still requires human workers for every adjacent function.

Amazon’s Agility Robotics Bet and the Warehouse Economics

Amazon’s acquisition of Agility Robotics in 2023 gave the company a vertically integrated path to deploying Digit — Agility’s bipedal robot — in Amazon fulfillment centres without the commercial uncertainty of a third-party supplier relationship. Digit’s warehouse deployment handles tote movement: picking up the wheeled shelf containers (pods) that Amazon’s Kiva/Amazon Robotics horizontal mobile robots bring to picking stations and returning empty pods to storage. This is physically demanding, repetitive work that creates injury risk for human workers and that represents a well-defined, bounded task for a bipedal robot equipped with arm dexterity and visual recognition. Agility’s commercial deployment story is on the Digit product page.

The Amazon fulfillment centre environment is not, however, the unstructured environment that humanoid robot proponents often invoke to justify bipedal over wheeled robotic systems. Amazon’s facilities are already heavily engineered around Kiva robotic shelving, with dedicated robot lanes, pod dimensions, and sensor infrastructure. Digit is operating in a partially structured environment, not a human-general one. The more relevant question is whether Digit’s capabilities in this constrained deployment can be extended to the genuinely unstructured picking tasks that human workers perform — selecting individual items from varied positions across the facility — and on that question, Boston Dynamics’ logistics deployment work and all competing platforms acknowledge that general-purpose picking at Amazon’s throughput rates remains beyond current humanoid capability.

Where Tesla Optimus Actually Stands in 2026

Tesla’s Optimus programme has not met Elon Musk’s publicly stated production targets. The goal of producing 1 million Optimus units by 2025 was not achieved; by mid-2026, Tesla has produced several thousand Optimus Gen 3 units, the majority deployed within Tesla’s own Gigafactory operations performing tasks that Tesla has not fully disclosed. The programme has demonstrated meaningful mechanical improvement — Optimus Gen 3 moves more naturally than the Gen 1 demonstration and handles smaller objects with more reliability — but it has not yet been commercialised in any confirmed third-party deployment.

The Optimus positioning remains strategically ambiguous: it is simultaneously a proof of Tesla’s manufacturing and AI capabilities, a potential future product line, and a demonstration platform for Tesla’s Dojo training infrastructure. The AI capex environment that has driven Nvidia, Microsoft, and Google to record infrastructure investment has not yet produced the training data infrastructure at humanoid-robot scale that would be required to match human task generalisation. Enterprise AI deployment at scale in knowledge work contexts has demonstrated that AI capability advancement is fast; physical embodiment introduces hardware constraints that software timelines do not.

The Commercial Reality Behind the Wave

The honest accounting of humanoid robot commercialisation in 2026 is that the technology has crossed the threshold from laboratory to production deployment for specific, bounded tasks in controlled industrial environments — and has not crossed the threshold for general-purpose use in unstructured environments. The Figure-BMW and Amazon-Agility deployments are real, commercially structured, and represent genuine milestones. They are not the all-purpose manufacturing and service labour substitution that the most optimistic projections have described.

The economic case for humanoid robots in 2026 requires the deployment to be in a high-labour-cost environment, performing a task that is physically repetitive and well-defined enough to fall within the robot’s current capability envelope, with a facility operator willing to pay the RaaS premium for a technology that is still evolving. The number of deployments meeting all three conditions is growing but remains small. The companies that will determine whether the category reaches mass commercial scale — Figure, Agility, Boston Dynamics, 1X, Apptronik — are all in the window between proof of commercial viability and proof of economic scalability, which is where most industrial robotics categories have historically either consolidated rapidly or stalled for a decade.

Where the Economic Gains From Humanoid Robots Actually Land

Every announcement of a humanoid robot deployment in a BMW facility or an Amazon fulfillment centre generates coverage that frames the development as a technology capability story: how far the robot has advanced, what tasks it can now perform, how it compares to prior demonstration units. The more consequential story — and the one that will define the category’s social and political implications over the next decade — is about economic distribution. When a humanoid robot replaces a task previously performed by a human worker, where does the value that worker was producing actually go? In the Robot-as-a-Service model that Figure AI, Agility Robotics, and Boston Dynamics are all building toward, the answer is primarily to equity holders — the investors and, eventually, shareholders of the robotics company — and secondarily to the enterprise customer capturing the margin between the RaaS subscription cost and the labour cost it is replacing.

Scott Galloway’s consistent observation about technology-driven displacement is that the US innovation economy has proven extraordinarily effective at creating wealth and structurally inadequate at distributing it. The Kiva mobile robotic system that transformed Amazon warehouse operations did not reduce Amazon’s warehouse headcount — Amazon’s warehouse employment grew substantially alongside its robotic deployment. But it fundamentally changed the composition of that workforce: less skilled physical movement, more monitoring, maintenance, and exception handling around robotic systems. The workers best suited to the pre-robotic warehouse had their most relevant skills partially devalued; the workers best suited to the post-robotic warehouse were different people with different training backgrounds. The transition produced more economic value at the aggregate Amazon level and produced disruption at the individual worker level that the headline job-count figure did not capture.

Humanoid robots at BMW and Amazon in 2026 are performing tasks that map exactly onto this pattern: physically demanding, repetitive work concentrated in manufacturing and logistics facilities in regions where alternative employment options are limited. The Spartanburg, South Carolina automotive corridor and the network of Amazon fulfillment centres in non-coastal markets are not places where workers displaced by humanoid robots can easily transition to the higher-skill roles that robot maintenance and oversight require. The technology’s commercial success — which is real, if still narrow in scope — will be measured in shareholder returns and corporate margin improvements. The question of whether those gains produce outcomes for the communities where the robots operate is not a technology question. It is a policy question that the industry’s promotional framing consistently presents as secondary, if it is presented at all.