Apple Is Talking to Intel About Making Its Chips in the US. The Market Just Priced the Entire Semiconductor Onshoring Trade in One Day.

Intel stock gained 13–15% on May 5, 2026, hitting a new all-time high, after Bloomberg reported that Apple has held early-stage exploratory discussions with Intel and Samsung about manufacturing the main processors for its devices in the United States. The move would make Intel and Samsung secondary options alongside Apple’s longtime manufacturing partner TSMC — and it would represent the most significant validation of Intel’s foundry revival that any single customer announcement could provide.

The talks are early. No orders have been placed. The same demand pressure driving these talks shows up across the semiconductor industry’s $1 trillion year and inside China’s 70% wafer self-sufficiency target, both of which sharpen the strategic case for any non-TSMC capacity Intel can credibly stand up. Apple has expressed internal concerns about using non-TSMC process technology and may not ultimately proceed with either Intel or Samsung. But the market didn’t price the certainty of an Apple order — it priced the credibility of the US semiconductor onshoring narrative finally having a customer willing to consider paying the premium to make chips in America.

That narrative has been the dominant policy trade in tech equities for two years and has been conspicuously short of hard commercial validation. Trump tariffs — the largest US tax increase as a percentage of GDP since 1993, costing the average household $1,500 in 2026 — have created structural pressure on any company with a Taiwan-concentrated supply chain. Apple has a more Taiwan-concentrated supply chain than almost any other company on earth. If Apple is seriously exploring alternatives, the pressure is real enough to move procurement decisions at the highest level.

What Intel’s Foundry Business Has Built to Receive This

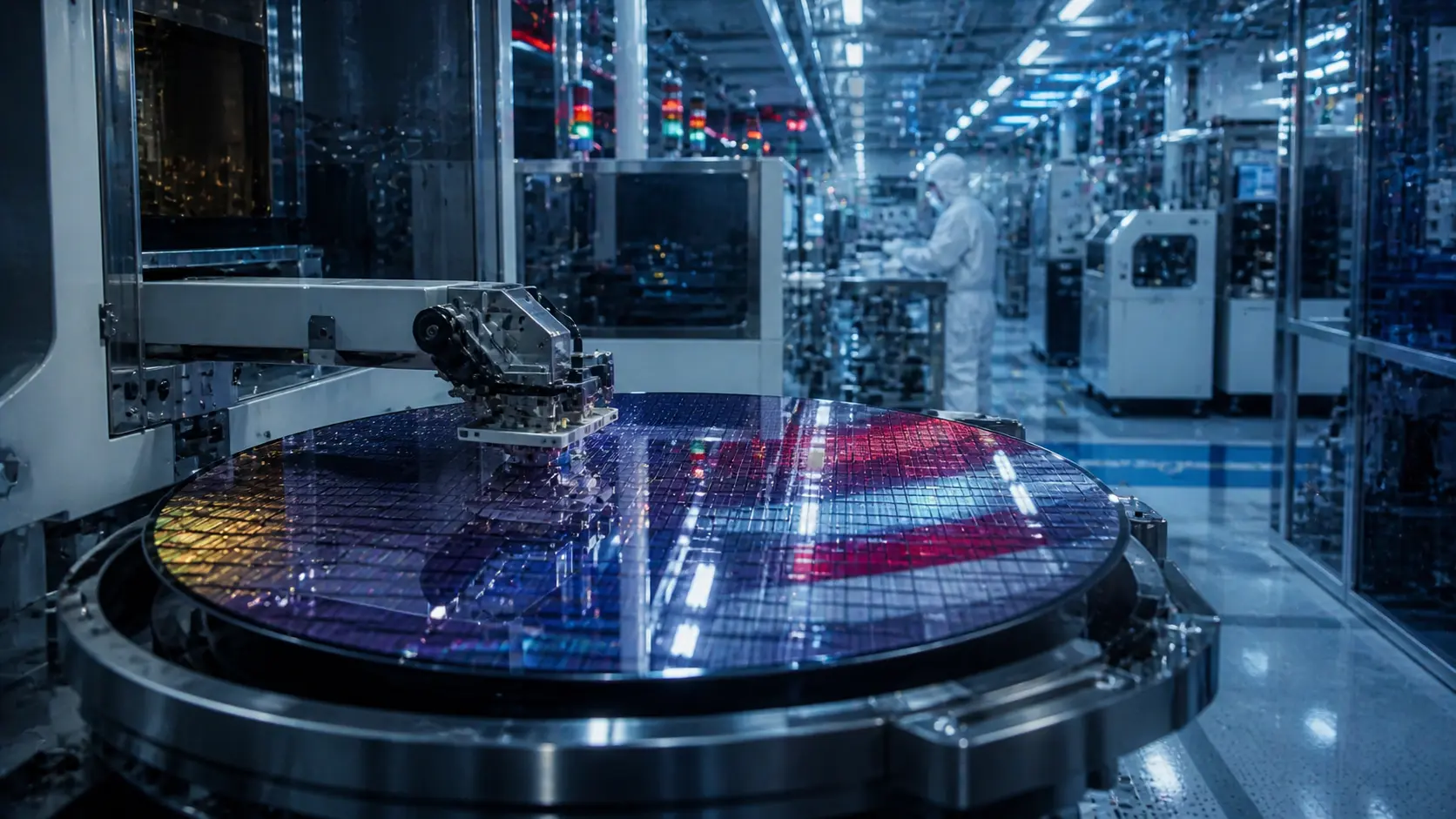

The Apple talks would have been meaningless six months ago. Intel’s foundry business was not capable of manufacturing Apple’s leading-edge processors at competitive yields. What changed is that Intel’s 18A process node has entered high-volume manufacturing — making Intel the only US-headquartered company operating a leading-edge semiconductor fabrication process at commercial scale.

Intel’s foundry revenue rose 16% year-over-year to $5.4 billion in Q1 2026 — a sharp acceleration from approximately 4% growth in Q4 2025. That acceleration reflects actual customer wins, not pipeline announcements. The most significant is Tesla’s agreement to use Intel’s 14A process for Elon Musk’s Terafab AI chip complex in Austin, Texas. Tesla is Intel’s first major external customer for the 14A node — the next-generation process beyond 18A — and the partnership confirms that Intel’s advanced foundry technology is credible enough for a company whose compute requirements are among the most demanding in the world.

Apple executives have made site visits to Samsung’s fab under development in Taylor, Texas — the same general geography as TSMC’s Arizona expansion. The site visit pattern matters: Apple does not send executives to look at fabs it has no intention of ever using. The visit may ultimately lead to nothing, but it is a data signal that Apple’s procurement teams are building relationship and process knowledge with US-based alternatives rather than simply committing to TSMC by default.

Intel’s all-time high on May 5 reflects a stock that has already had an extraordinary 2026. Intel is up approximately 175% year-to-date in 2026, with the bulk of gains coming as the foundry revival thesis moved from roadmap to execution. The May 5 move added a market-cap figure larger than many mid-cap companies in a single trading session, on a news item that explicitly described discussions at an early stage with no commitment made. That is not irrational exuberance — it is the market re-rating the probability distribution of Intel becoming a credible foundry for the world’s most valuable hardware company.

The Tariff Architecture Behind the Supply Chain Shift

Understanding why Apple is looking at US-based chip manufacturing requires understanding the tariff structure that makes Taiwan-only supply chains financially untenable at scale.

The current US tariff regime includes aggressive duties on imports from Taiwan and South Korea as part of broader trade policy. For Apple, which imports finished devices and components manufactured almost entirely in Asia, the tariff burden compounds across multiple supply chain layers. A chip manufactured in Taiwan, assembled into an iPhone in China or Vietnam, and imported into the US faces tariff exposure at each stage that eventually hits the consumer price — or Apple’s margin.

Apple has publicly committed to over $600 billion in US manufacturing investment over four years. In 2026 alone, Apple is on track to purchase more than 100 million advanced chips from TSMC’s Arizona fab — TSMC has pledged $165 billion across its first three Arizona fabs, with the first already in production and the second and third set for 2027 and end of decade. The TSMC Arizona expansion is the primary answer to Apple’s US manufacturing commitment. The Intel and Samsung discussions are the contingency planning for what happens if TSMC Arizona cannot scale to Apple’s full chip volume within the required timeline.

The broader market backdrop on May 5 reflected a macro environment where the onshoring trade is working. The S&P 500 closed at a new all-time high of 7,259.22, gaining 0.81%, while the Nasdaq gained 1.03% to 25,326.13 — also a record. Tech was the best-performing S&P 500 sector on the day, adding over 2%. Falling oil prices provided an additional tailwind: WTI crude dropped 3.9% to $102.27 on Iran de-escalation, removing a macro headwind that had pressured consumer spending estimates through April. The combination of record equities, a tech-led rally, and the Intel news created a single-day snapshot of the bull case for the US industrial renaissance trade.

What This Means for Bitcoin Miners and the Crypto Compute Supply Chain

The semiconductor onshoring story has a direct and underappreciated connection to the crypto industry through two channels: Bitcoin mining hardware and AI compute infrastructure.

Bitcoin mining is a semiconductor-intensive industry. ASIC chips — application-specific integrated circuits designed exclusively for SHA-256 hashing — are manufactured almost entirely in Asia, predominantly by Bitmain and MicroBT using TSMC and Samsung foundry capacity. US-based Bitcoin miners including Marathon Digital, CleanSpark, and Riot Platforms are entirely dependent on Asian semiconductor supply chains for the hardware that generates their revenue. A geopolitical disruption to Taiwan — the exact scenario that TSMC’s Arizona expansion and Intel’s foundry revival are designed to hedge against — would immediately halt ASIC production and create supply shortages that could last 12–18 months at the scale of new fab construction.

Intel’s 18A and 14A process nodes are sufficiently advanced to manufacture ASIC-class compute chips. Tesla’s Terafab AI chip is the proof point — a custom AI accelerator being manufactured at Intel’s leading-edge nodes is structurally similar in design complexity to a Bitcoin mining ASIC. A US-domiciled, Intel-manufactured Bitcoin mining chip is technically feasible under the same foundry infrastructure that the Apple talks have now validated as commercially serious.

The Decentralized Physical Infrastructure (DePIN) narrative that has driven significant crypto venture investment in 2025–2026 is also directly connected to semiconductor geography. DePIN networks — decentralised compute, storage, and wireless infrastructure — explicitly argue that concentrating physical compute infrastructure in a small number of geographic locations creates censorship and disruption risk. The US semiconductor onshoring push is the macro-level version of the same argument. Intel’s foundry revival reduces the single-point-of-failure risk in the global semiconductor supply chain in exactly the way DePIN projects argue decentralised infrastructure reduces the single-point-of-failure risk in digital infrastructure.

Samsung’s 5.4% Gain and What the Korean Trade Signals

Samsung gained 5.4% to close at a record KRW 232,500 in Seoul trading on May 5 — a meaningful move for a company with Samsung’s market capitalisation, and a signal that the market read the Apple talks as credible enough to reprice both potential foundry partners simultaneously.

Samsung’s Taylor, Texas fab is the facility Apple executives have been visiting. Taylor is approximately 30 miles northeast of Austin — in the same general technology corridor as Tesla’s Terafab, AMD’s Austin R&D operations, and a growing cluster of semiconductor supply chain companies that have relocated to Texas specifically because of the CHIPS Act incentives and the concentration of advanced manufacturing investment in the region.

Samsung’s Taylor fab is designed for advanced-node production — 2nm and below — and has received CHIPS Act funding from the US federal government. If Apple were to place orders at the Taylor facility, Samsung’s fab would become one of the most commercially significant semiconductor manufacturing facilities in the US. The market is pricing in the optionality of that outcome, not the certainty of it.

The Fed’s most recent meeting — a hold at 3.50–3.75% on April 29 — produced the most divided vote since October 1992, with four dissents. Governor Stephen Miran dissented in favour of a 25bp cut; Hammack, Kashkari, and Logan dissented in favour of removing the easing bias from the statement. A four-dissent FOMC under Powell means the interest rate outlook is genuinely contested within the committee — which typically translates to rate volatility and a bias toward assets with hard supply caps, including Bitcoin. The semiconductor story and the monetary policy story are not unrelated: both are downstream of the same tariff-driven macro uncertainty — operating alongside the Magnificent Seven $700B AI capex cycle — that is reshaping US industrial policy and institutional portfolio construction simultaneously.

Tokenised Equities and the Intel Trade

Intel’s 175% year-to-date gain and all-time high are directly accessible to crypto-native investors through tokenised equity platforms that have launched on Solana and Base over the past 18 months. Platforms offering 24/7 on-chain trading of tokenised US equities — including major tech stocks — have experienced significant volume growth in 2026 as institutional investors and retail crypto users access equity exposure through crypto wallets rather than traditional brokerage accounts.

The Intel trade on May 5 was precisely the kind of event-driven move that tokenised equity platforms are designed to capture. A 13–15% single-day move in a major US stock, driven by a news event that broke during Asian trading hours, is accessible to crypto-native investors in markets where traditional equity exchanges are closed. The 24/7 on-chain equity thesis — that global investors should be able to trade US stocks at any hour without a brokerage account — is demonstrated most clearly by the market-moving events that occur outside of traditional trading hours.

The broader market record on May 5 — S&P 500 and Nasdaq at simultaneous all-time highs — reflects an equity market that is pricing in the US industrial renaissance thesis with increasing conviction. For crypto, the connection is through the institutional portfolio construction that tends to increase crypto allocation when equities are at records and risk appetite is high. Bitcoin’s $2.44 billion April ETF inflow surge and its $80,000 break on May 4 occurred in exactly this macro environment — and the semiconductor onshoring story that drove May 5’s equity record is the same structural narrative that supports institutional digital asset allocation over the 12–24 month horizon.

A Hand-Built Visit Through The Fab That Apple Is Considering

Inside an Intel fab in Arizona — the specific one the Apple conversations are reportedly about — the work has a texture that the supply-chain conversation flattens. The cleanrooms run at a humidity level the maintenance log specifies to one decimal place. The tools are calibrated daily, then verified weekly, then audited monthly, with paper records kept alongside the digital ones because both have failed at separate points in the fab’s history. The engineers who walk the floor describe the rhythm in the same phrase used by carpenters and chefs: it is the kind of work where consistency is the entire game, and where the difference between a yield rate of 70% and 73% is the difference between a profitable line and an unprofitable one.

This is what Apple is evaluating when its supply chain team flies out for the visit. Not the announcement-shaped story. The yield consistency over the previous six quarters. The maintenance discipline visible in the way the floor is kept. The specific way the Intel team responds when a non-standard process question gets asked — whether they say “we have not tried that” or “we tried that in 2023 and here is why we stopped.” Apple has spent two decades learning to read fabs this way. The conversation that the headlines describe as preliminary is, on the floor, the most consequential customer audit the Intel foundry business has hosted in years.

The political layer around the visit — tariffs, reshoring, semiconductor policy — is real but downstream. What the engineers on the floor are doing is the layer that determines whether the policy outcome can be honoured. Both sides of the conversation know it. The headline will report on the policy. The decision will be made on the floor.

Frequently Asked Questions

What happened to Intel stock on May 5, 2026?

Intel (INTC) surged 13–15% on May 5, 2026, hitting a new all-time high after Bloomberg reported that Apple has held early-stage exploratory discussions with Intel and Samsung about manufacturing main device processors in the United States. The discussions are preliminary — no orders have been placed — but the report validated Intel’s foundry revival thesis at the highest possible commercial level. Intel is up approximately 175% year-to-date in 2026, driven by its 18A process node entering high-volume manufacturing and Tesla signing as its first major 14A customer.

Why is Apple considering moving chip manufacturing away from TSMC?

Apple’s Taiwan supply chain concentration has become a strategic liability under the Trump tariff regime — the largest US tax increase as a percentage of GDP since 1993 — which creates cost pressure on Taiwan-imported components. Apple has publicly committed to over $600 billion in US manufacturing investment over four years and is on track to purchase 100+ million chips annually from TSMC’s Arizona fab. The Intel and Samsung discussions represent contingency planning for additional US-based foundry capacity beyond what TSMC Arizona can deliver within the required timeline.

How does semiconductor onshoring affect Bitcoin miners?

US Bitcoin miners — including Marathon Digital, CleanSpark, and Riot Platforms — are entirely dependent on Asian semiconductor supply chains for ASIC mining hardware. A geopolitical disruption to Taiwan would halt ASIC production for 12–18 months at the scale needed to build new fab capacity. Intel’s leading-edge 18A and 14A nodes are technically capable of manufacturing ASIC-class compute chips — the same architecture as AI accelerators like Tesla’s Terafab chip. A US-domiciled Bitcoin mining chip supply chain is now technically feasible under the foundry infrastructure that the Apple talks have validated as commercially serious.

What did the S&P 500 do on May 5, 2026?

The S&P 500 closed at a new all-time high of 7,259.22, gaining 0.81% on May 5, 2026. The Nasdaq Composite gained 1.03% to a record 25,326.13. The Russell 2000 rose nearly 2%, also setting a new intraday record. Tech was the best-performing S&P 500 sector, adding over 2%, driven primarily by the Intel semiconductor move. Falling oil prices — WTI crude down 3.9% to $102.27 on Iran de-escalation — provided additional macroeconomic tailwind.

What is the connection between semiconductor onshoring and DePIN?

Decentralized Physical Infrastructure (DePIN) networks argue that concentrating physical compute, storage, and connectivity infrastructure in a small number of geographic locations creates censorship and disruption risk — and that decentralised alternatives reduce that risk. The US semiconductor onshoring push makes the same argument at the macro level: TSMC’s near-monopoly on leading-edge chip production creates a single-point-of-failure in the global technology supply chain that Intel’s foundry revival is designed to hedge. Both are expressions of the same underlying thesis about geographic concentration risk in critical digital infrastructure.

Sources

- Bloomberg: Apple Explores Using Intel and Samsung to Build Main Device Chips in the US (May 5, 2026)

- CNBC: Intel Soars 13% on Report of Apple Chip Talks, Hits New All-Time High

- Motley Fool: Intel Is Rocketing Higher on Reports of Apple Partnership (May 5, 2026)

- TechPowerUp: Intel Stock Surges to All-Time High on Foundry Revival and Strong CPU Demand

- TheStreet: Stock Market Today May 5, 2026 — Small-Caps and Tech Lead as Nasdaq and Russell 2000 Set Records

- Supply Chain Digital: TSMC’s $165B US Expansion Reshapes Global Chip Supply

- Tax Foundation: Trump Tariffs Tracker 2026 — Trade War by the Numbers

- CNBC: Fed Holds Rates Steady at 3.50–3.75% Amid Four-Way Dissent (April 29, 2026)

- DefiCryptoNews: Bitcoin Back Above $80,000 — $2.44B April ETF Inflows Explained

- VaaSBlock — Web3 risk and governance analysis

Intel Foundry Faces a Platform Governance Problem TSMC Never Had

Semiconductor manufacturing has historically operated as a utility business. TSMC built the world’s most advanced fabs and then, for two decades, stayed deliberately invisible inside the devices those fabs enabled. The value capture happened upstream and downstream — in the fabless design houses like Qualcomm and Apple and NVIDIA that owned the product relationships, and in the brands that sold to consumers. TSMC’s positioning was indispensable but not prominent. That was the point.

Intel’s foundry pivot asks something structurally different of the market: a company that has historically captured value through vertical integration — designing, making, and selling chips under its own brand — is now opening the factory floor to the companies it competes against. The Intel Foundry Services model requires Apple and other prospective customers to believe that Intel can separate its foundry relationship from its product rivalry. This is not a technology question. It is a platform governance question, and it is one TSMC has never had to answer because TSMC has never shipped a competing product.

For Apple, the calculus is about supplier diversification, not sentiment. Apple’s A-series chips are the company’s most important internal hardware advantage; handing that design work to an Intel facility requires Intel to demonstrate neutrality that its entire institutional history runs against. TSMC built that neutrality over decades through a single structural commitment: its only revenue comes from making other companies’ designs better. Intel’s foundry business will have to build equivalent trust while simultaneously doing the opposite. That is the governance problem Arizona’s infrastructure spending cannot solve — and it is the actual risk variable behind every public statement about U.S. semiconductor self-sufficiency.